Displaying present location in the site.

ICT Global Trend Part5 No.2

Rapidly expanding Fintech service in China 2/3

by Koichiro Ohira, Senior Fellow

1.3Billion Yen in P2P Financing

In the field of financing, the P2P (Pier to Pier)Lending is getting popular and focused where the direct financing transaction is being made on line platforms between companies or private users. The number of P2P lending platforms has been normalized and stable now as those illegal platforms acting fraudulent practices are regulated out.

The balance of P2P lending at the end of 2016 was recorded as 816.2 Billion RMB ( casi 1.3 Billion yen) doubling the balance of the year before. Chinese banks are prioritizing the lending to state-owned enterprises over the lending to the individual or private companies, so, the individuals or private companies are finding it difficult to borrow the money from the banks, and, are suffering from higher interest rate.

P2P Lending scheme is that there are no physical restrictions between lenders and borrowers and they can make financing transactions with relatively lower cost.

So the scheme is actually supplementing the lending transactions unsatisfied by banks to cover the demands though in small scale but in numerous numbers. and, is getting very essential infrastructure for financing transactions.

Revolutions over credit creation

So called “Micro Credit” is also getting popular that non-banking companies are lending small amount of money to the individuals and small and medium enterprises.

Most popular companies are MYBank in the Alibaba Group and WeBank in the group of Tencent. They seem to be utilizing the date obtained in the group such as transaction history of e-commerce, and the settlement accounts to judge how much credit can be given to the borrowers. We may say that these internet on-line financing schemes are changing the way how the credit is judged and given specially for the individuals and small and medium enterprises.

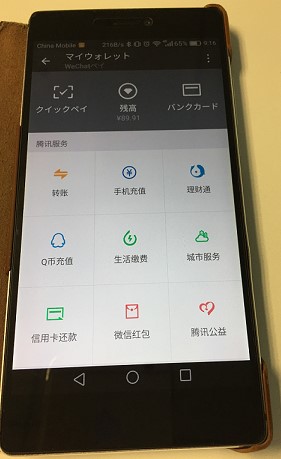

The smartphone is contributing positively to the deployment of these on-line financing schemes. For example WeChat Pay by Tencent offers a variety of applications on the smartphone such as QR Code payment, Small Investment scheme, WeBank and further more, new year gift money transfer , donation transfer, payment of living expenses such as water or lighting, reservation of hospital and flight, theater ticket and so on.

These applications are offered all on the smartphone.

WeChat is used by 889million users at the end of 2016, and, a variety of financing services are all prepared and ready for use on the same application for such a large number of users.

“All in One” Offer

Not only in China but also in developing countries where banking and financing infrastructures such as branch offices and ATM are not well deployed the smartphone can be the essential tool to support financial transactions. We can easily imagine that new business models will be developed to offer “All in one” type of internet on-line financing services like Alibaba and Tencent in China.

On the other hand Japan has well developed banking and financial infrastructures who offer very high level of services, so, it may be difficult for new comer to offer “All in One” financing services and to gain the share in this banking field. It has to be mentioned that even in Japan such demand and request would be increased more for better and convenient financing services to be enjoyed by ordinary people like artificial “All in One” applications shared among related companies.