Displaying present location in the site.

ICT Global Trend Part7-1

Challenge of InsurTech in USABenefits both for policy holders and insurance company

This article is written by Mr.Koichiro Ohira, Chief Fellow, Institute for International Socio-Economic Studies(NEC Group)

USA, the largest insurance market in the world

USA is the largest insurance market in the world with total annual insurance premium revenue exceeding one trillion dollars.

USA is also the global leader in the world of InsurTech employing advanced ICT technologies in the insurance sector such as AI (Artificial Intelligence) , IoT (Internet of Things) and mobile devices.

Many start-ups are actively and largely contributing to the development of InsurTech, same as in the area of Fintech (fusion of Finance and Information Technology) in the State of California with famous Silicon Valley and in the New York State with global financial center.

Amount of venture capital Investment to such InsurTech start-ups is globally in increasing tendency and most of such investment are made to American start-ups.

Start-ups seldom arrange their own insurance service for consumers and enterprises, but, are in most cases collaborating with existing insurance companies to be partly responsible for the insurance work process.

Discount of Insurance Premium

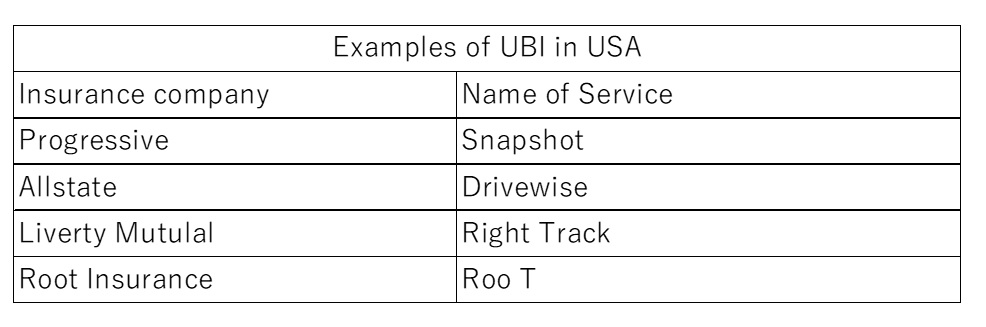

If we look at each vertical category, we can see that in the car insurance category UBI (Usage Based Insurance) is the most popular where policy holders can enjoy the discount premium if they are judged driving safe by records of driving speed, timing of brake, driving time zone and driving distance measured by the sensor equipped at the car.

Sensor, however, should not necessarily be the one designed specially for the purpose. Lately such UBI are newly offered in the market as can obtain and analyze driving information easier from normal GPS (Global Positioning System) function of smart phone and accelerometer.

If we advance the concept of UBI, there appears in the market such insurance company who offers car insurance with variable insurance premium “Pay-Per-Mile” in accordance with the driving distance. In this area MetroMile is popular and famous start-up.

Such driving information as obtained through specialized sensor and smart phone can be fed back to policy holders (or drivers) via smart phone applications so that the they can be well informed of their driving manner and can reduce the risk of accidents.

In this smart phone application the policy holders can monitor driving record and fuel consumption records as well so that they can appreciate also how close the insurance works for them.

Substituting Damage Assessment

It is getting more and more popular that the policy holders can substitute the damage assessment work of damage investigator by taking photo of damaged part and whole of the car by smart phone and sending those photos to the insurance company for assessment.

This method can substantially shorten the time needed from the accident to the actual payment of insurance money together with the arrangement of cashless payment.

As explained above, in USA they are actively working to reduce the cost of insurance company as well as to offer benefits to policy holders by reducing the number of accidents and reducing annoying process of insurance applications with the utilization of InsurTech.

In the next issue it will be reported how IoT devices are used at home and how wearable devices are utilized.